Personal Banking

Personal Banking

Quarterly Perspectives - 2nd Quarter 2025

As we enter the second quarter of 2025, our Quarterly Perspectives dive deeper into a variety of current topics. Read on to learn more about creating a wealth purpose statement, donor-advised funds, Social Security and retirement age, market volatility, and more.

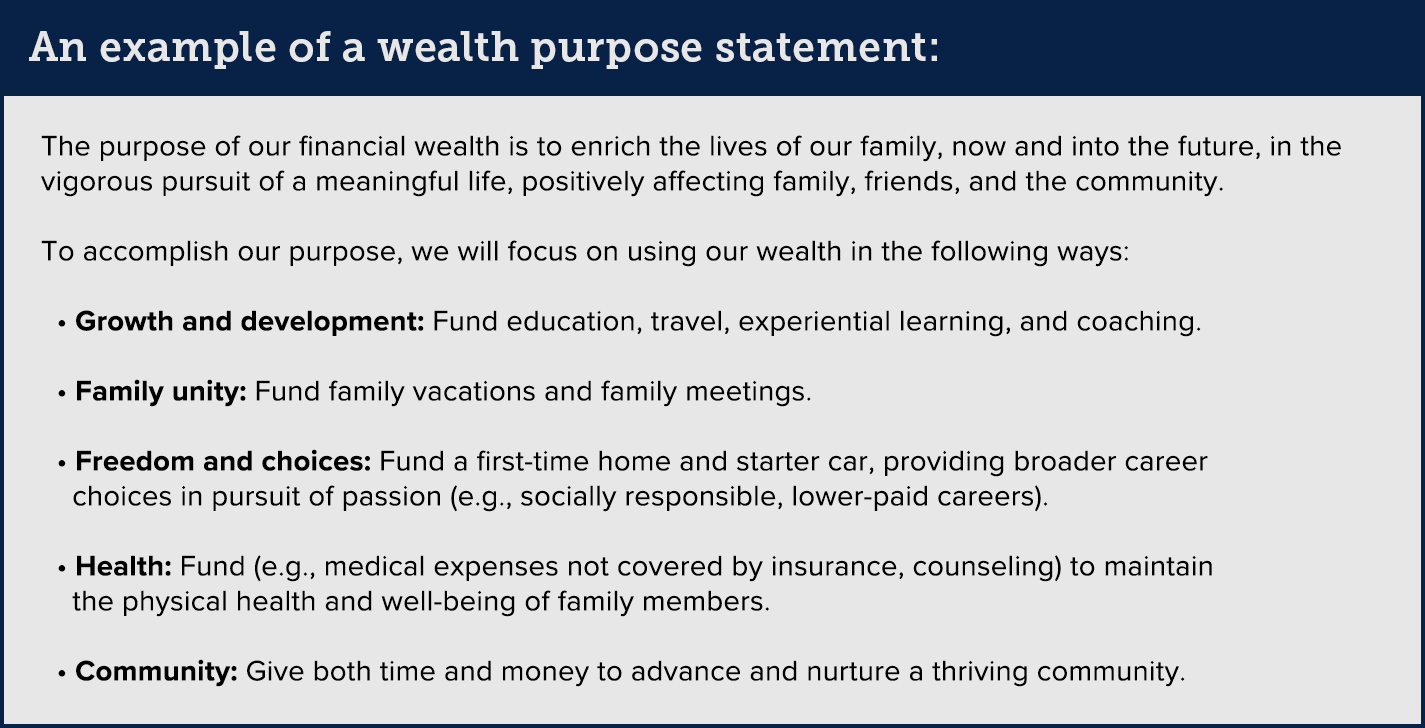

ESTATE PLANNING – What is your generational wealth strategy?

With wealth comes responsibility and potential for fulfilling purpose. Do your heirs understand your views on wealth and your desires for your estate? The following activity is designed to help you determine purpose for your wealth.

- Brainstorm: List the potential opportunities created by financial resources.

- Identify: Highlight or circle the opportunities most important to you.

- Evaluate: Determine what themes are emerging from your priorities.

- Outline: Reflect on the themes and draft a purpose statement for your wealth.

- Plan: Construct a course of action to move your purpose forward.

- Safeguard: Be mindful of any potential pitfalls or roadblocks as you pursue your purpose.

- Involve: Have your partner and mature family members walk through the same process, and then create a shared Wealth Purpose Statement together.

- Discuss: Communicate your purpose and values to younger family members as teachable moments.

CHARITABLE PLANNING – Is a donor-advised fund (DAF) right for you?

Discover a flexible and tax-efficient way to manage your charitable giving.

A DAF may be right for you if:

- You had a high-income year. A DAF could help you offset taxable income from bonuses, business sales, or stock options.

- You own appreciated assets. A DAF could help you donate securities or real estate to avoid capital gains taxes and get full market value deduction.

- You are planning for the future. A DAF could help you create a lasting charitable legacy that can involve your family.

- You give regularly. A DAF could help you simplify and organize your charitable contributions over time.

Source: Ren

TAX PLANNING – Take advantage of a down market for Roth conversions

If you are considering a Roth conversion, a down market may present an opportunity for you.

- Lower tax cost: When you convert to a Roth IRA, you pay taxes on the current value of the assets being converted. If the market is down, the value of your assets is lower, meaning you’ll pay taxes on a smaller amount.

- Convert a larger portion: By paying taxes on a lower value, you can effectively convert a larger portion of your account for the same tax cost.

- Tax-free growth: Once converted to a Roth IRA, any future growth is tax-free, which can be a significant benefit, especially if you anticipate higher tax rates in the future.

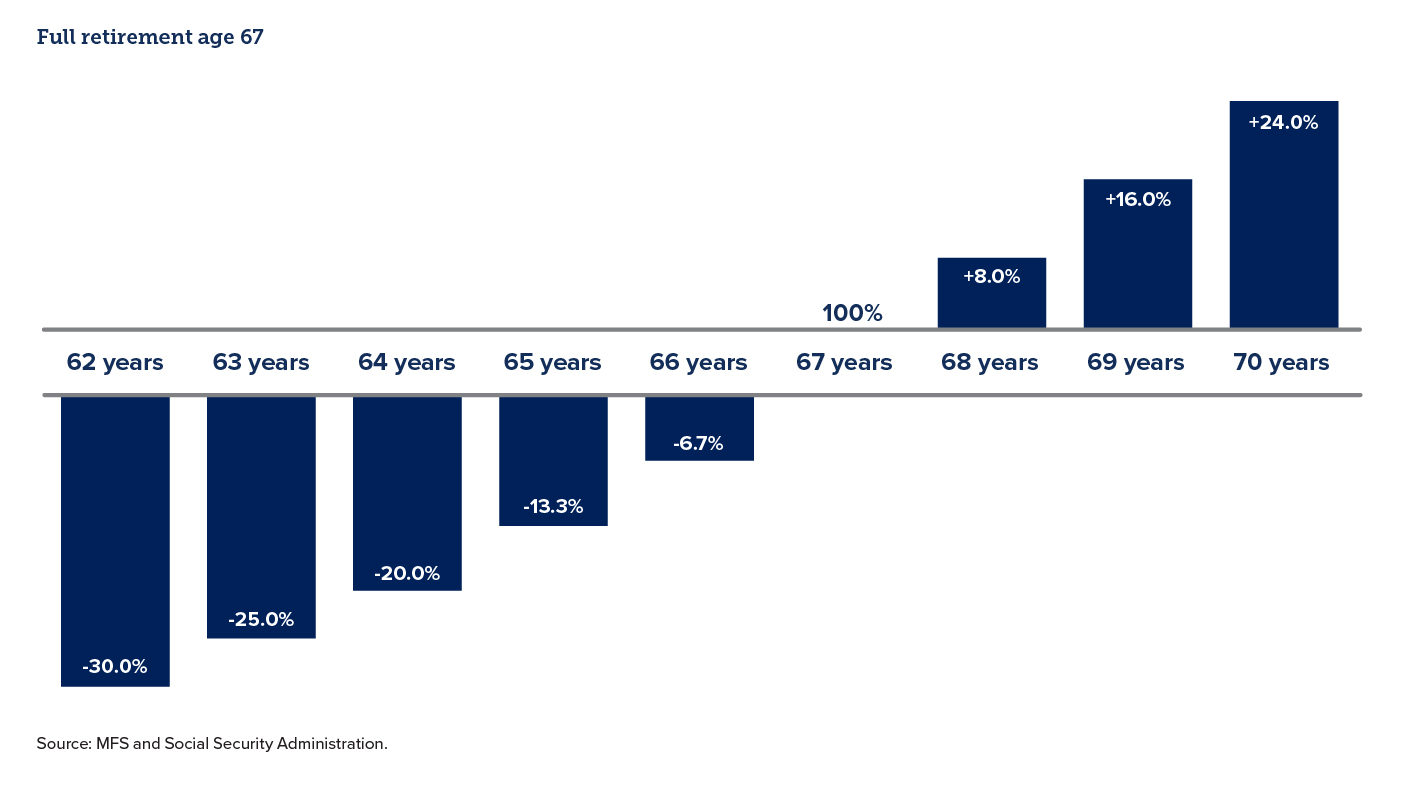

FINANCIAL PLANNING – The age you start Social Security matters

- Starting Social Security either before or after your full retirement age (FRA) will have a significant effect on your benefit.

- Reduced or increased monthly payments will follow you for the rest of your life and possibly your spouse’s life as well.

- Starting Social Security prior to your FRA could also affect the amount your spouse will receive.

- Your Advisor can help you model the effects of taking Social Security at different ages.

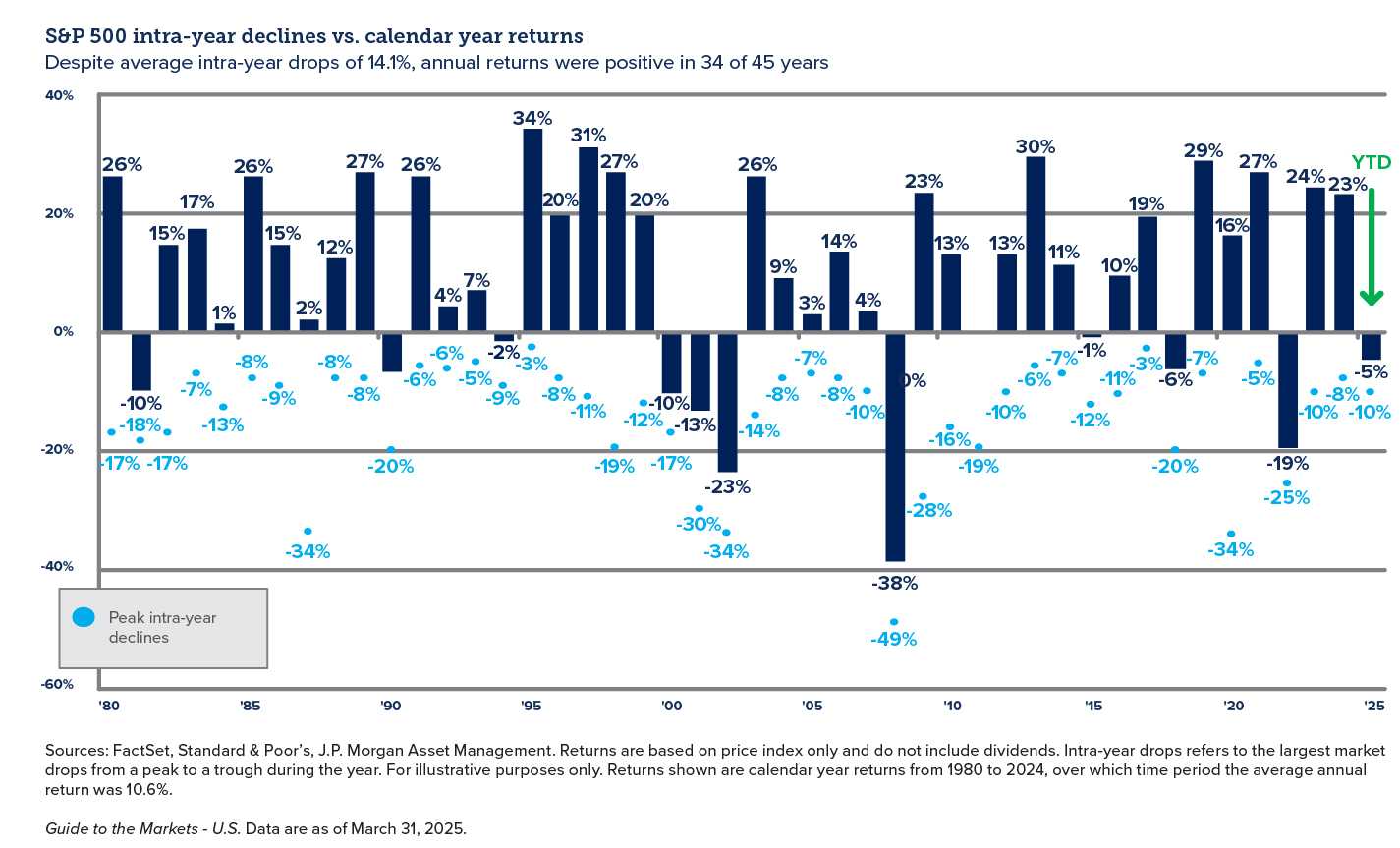

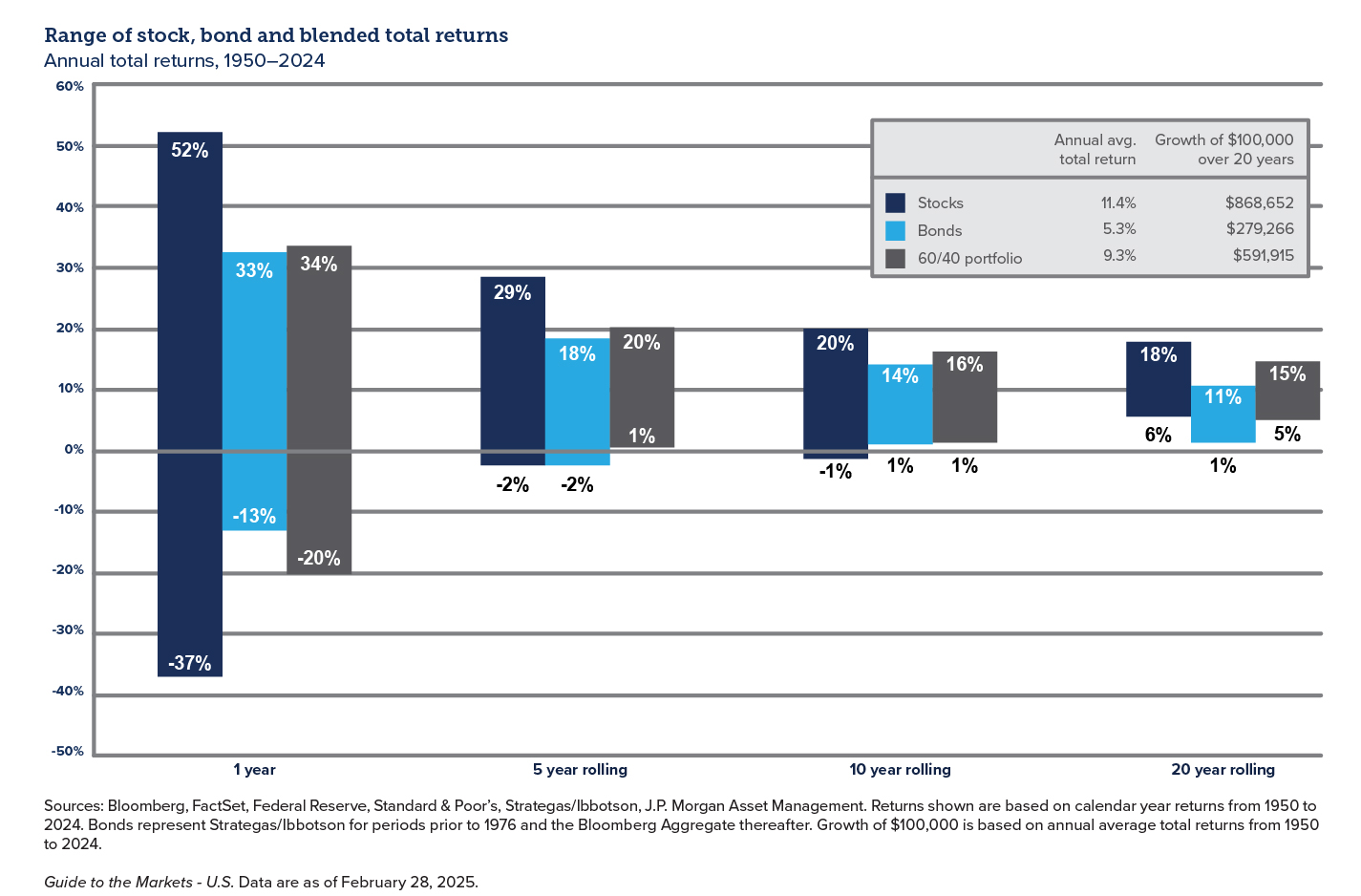

Market volatility is always present, even in the good years

- Short-term market volatility is heavily influenced by negative headlines – such as geopolitical conflicts or financial crisis – but the effects tend to be short-lived.

- Despite average intra-year drops of 14.1%, annual returns were positive in 34 of 45 years.

- On average, the S&P 500 experienced an intra-year drop of 15% or more every 2.5 years.

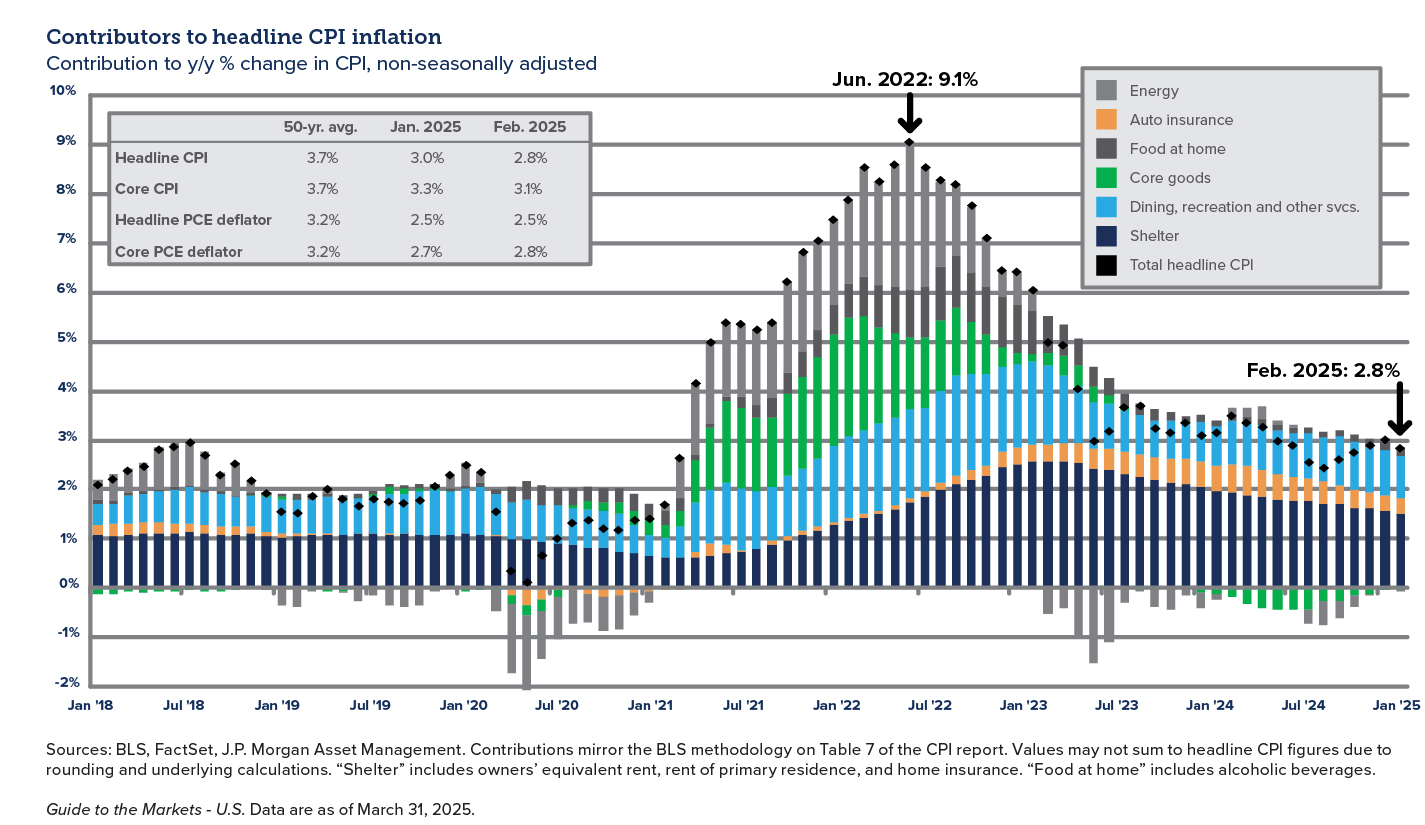

Inflation improving but remains a concern

- Headline inflation has shown a significant drop from the highs experienced in Summer 2022, but the Fed remains committed to their 2% target.

- “Sticky” inflation components, such as the cost of shelter, will likely remain a dominant driver of overall inflationary pressures.

- Effects of potential tariffs remain unknown but will likely add upward pressure to many inflation components.

Time, diversification, and the volatility of returns

- The prudent investor knows that it is time in the markets, not timing the markets, that matters.

The INTRUST Quarterly Perspectives are the consensus of the INTRUST Investment Strategy team and are based on third-party sources believed to be reliable. INTRUST has relied upon and assumed, without independent verification, the accuracy and completeness of this third-party information. INTRUST makes no warranties with regard to the information or results obtained by its use and disclaims any and all liability arising out of the use of, or reliance on, the information. The information presented has been prepared for informational purposes only. It should not be relied upon as a recommendation to buy or sell securities or to participate in any investment strategy. The Quarterly Perspectives are not intended to, and should not, form a primary basis for any investment decisions. This information should not be construed as investment, legal, tax or accounting advice. Past performance is no guarantee of future results.

| Not FDIC Insured | No Bank Guarantee | May Lose Value |

Posted:

04/23/2025

Category:

Related Blog Posts