In our 2025 Economic Outlook, we evaluate the current economic environment and its implications for businesses and investors. Key themes shaping this year's outlook include economic growth, consumer confidence, job market, tariffs, debt and tax policy, global tensions, deregulation efforts, and more.

U.S. economy

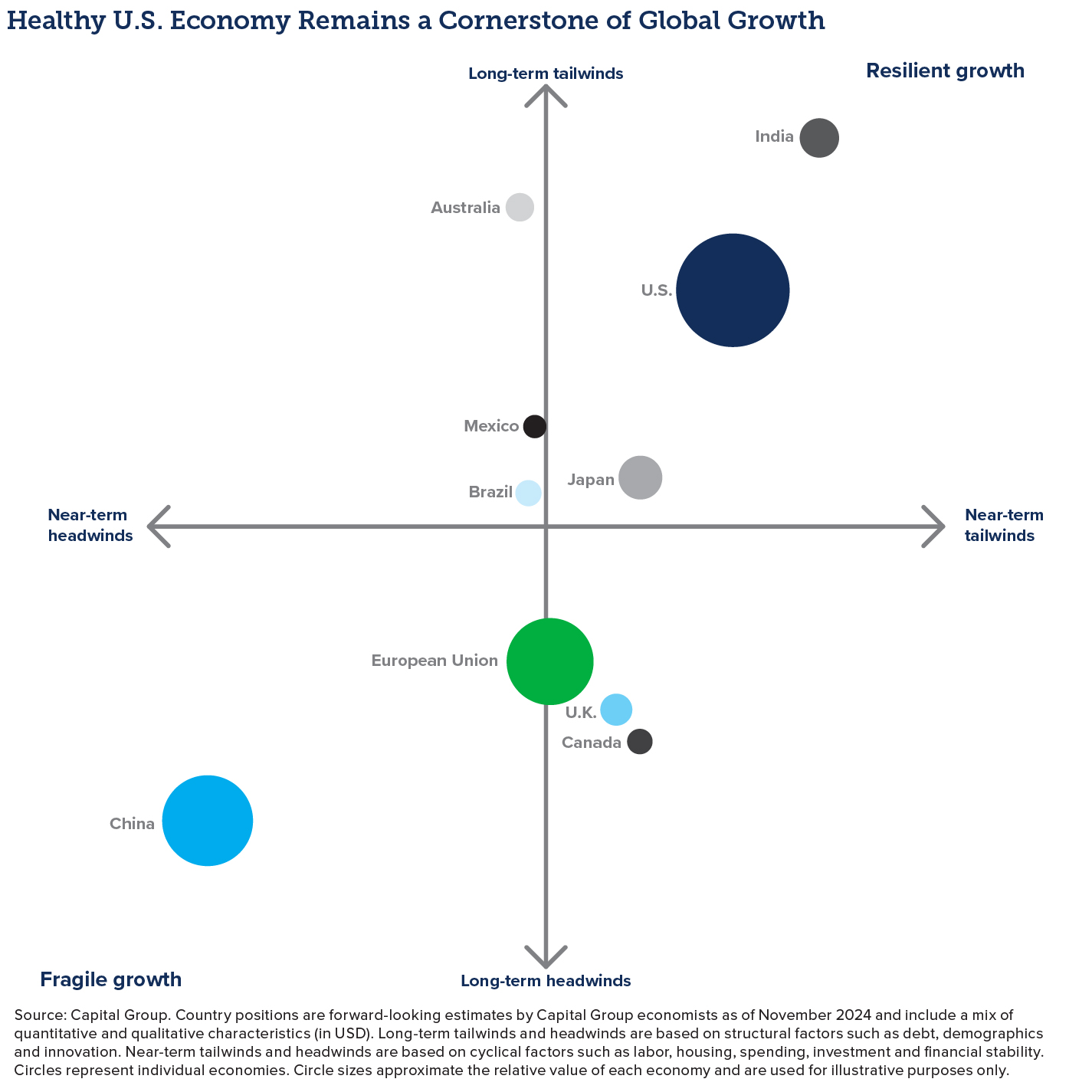

Positive growth continues

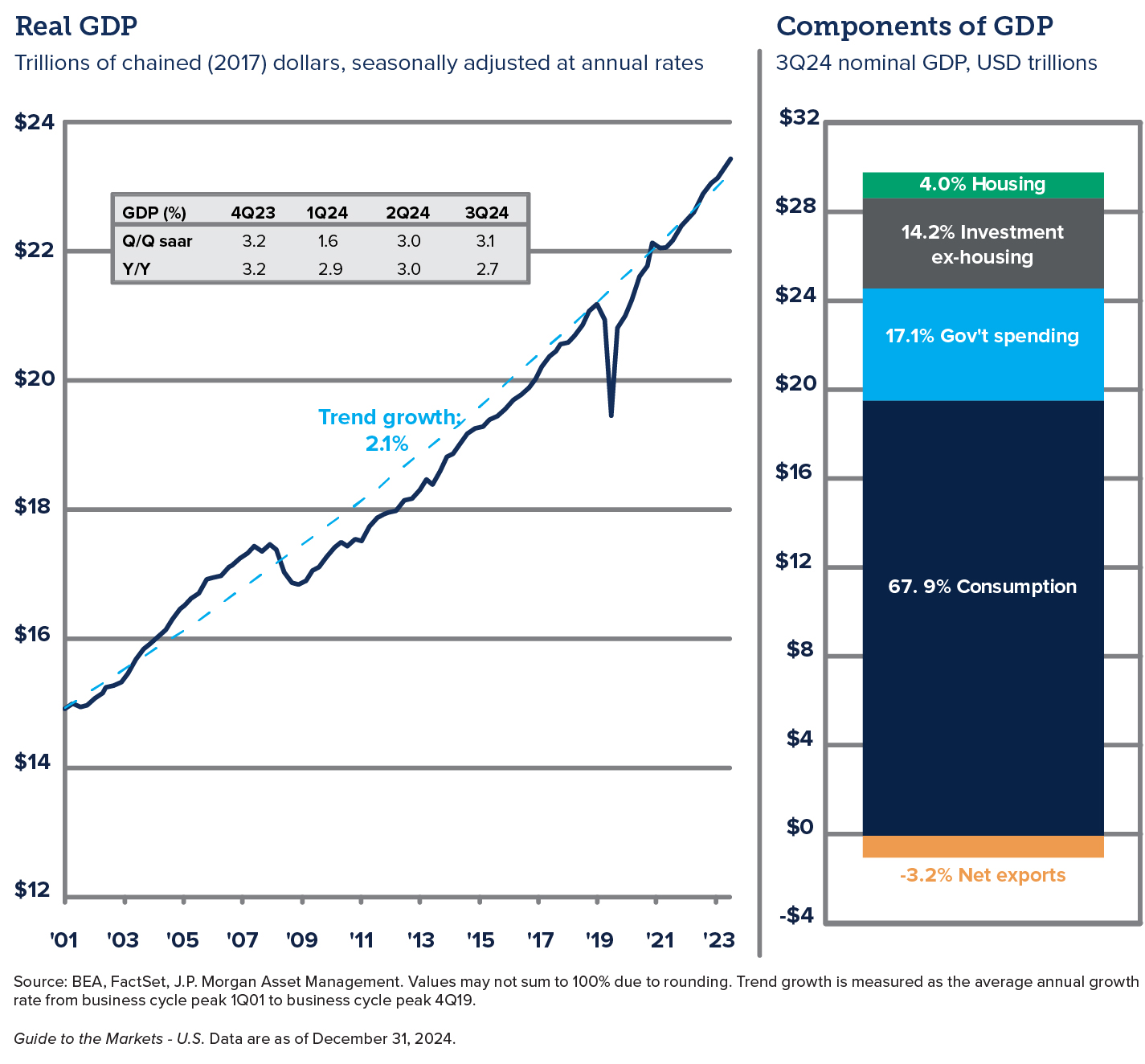

Our outlook for the financial markets and the U.S. economy this year remains positive. The strong growth experienced in 2024, with real GDP growth slightly above trend, has alleviated concerns about a potential recession. The new administration, along with the current composition of Congress, is expected to focus on stimulating economic growth through tax cuts and deregulation. However, initiatives such as immigration reform and targeted tariffs on foreign goods and services could pose challenges to this growth.

Economic growth and job market

While real GDP is projected to remain largely unaffected in 2025, the tax cuts likely to take effect at the start of 2026 could pull forward capital spending into 2025. The labor market may face tightening as immigration policies are implemented, potentially impacting job growth. Despite these challenges, consumer confidence remains above average, supported by strong household balance sheets, falling inflation, and real income growth.

Consumer confidence

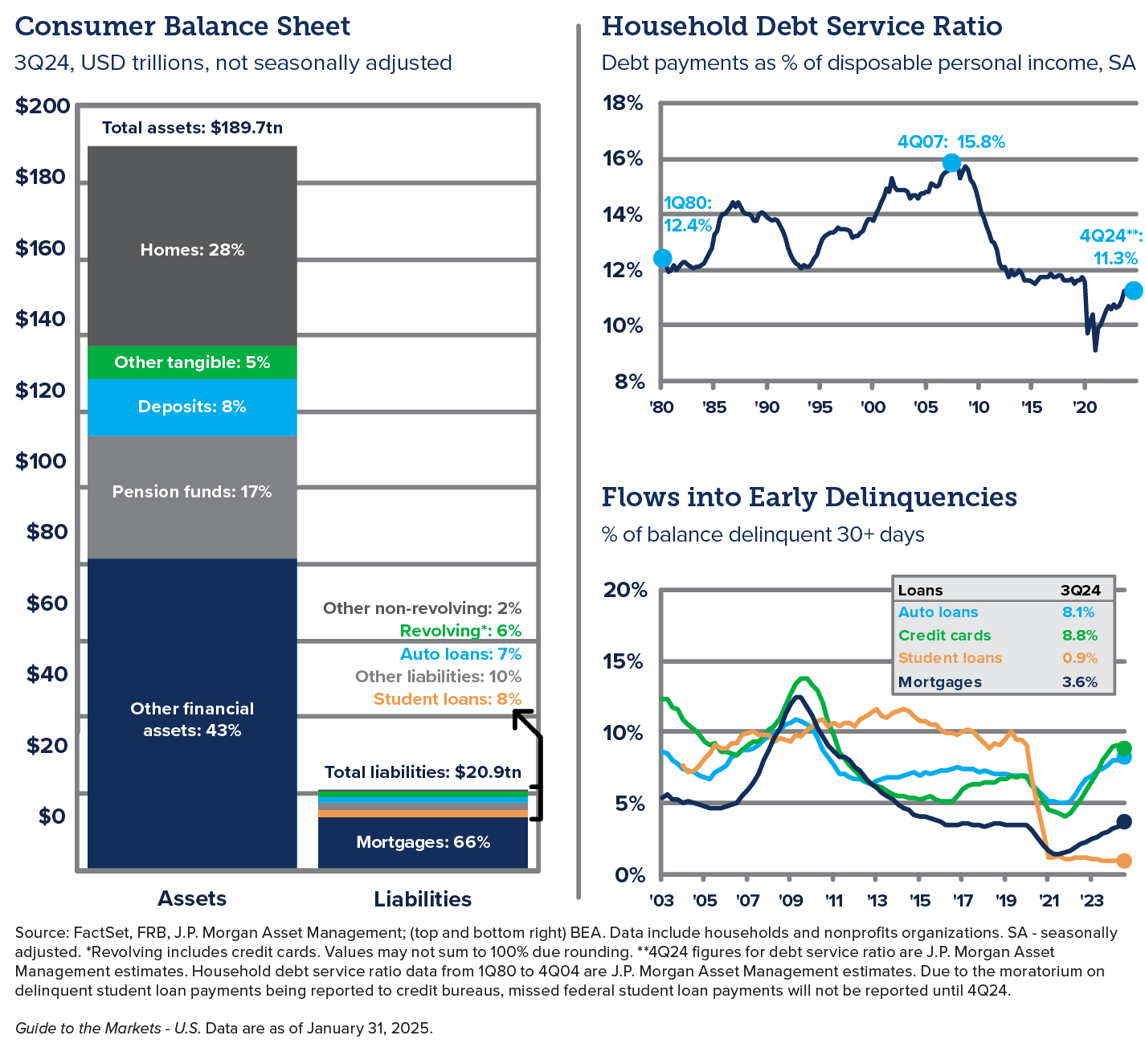

Consumer confidence is a critical factor in our positive outlook for 2025. High consumer confidence is driven by several key factors, including strong household balance sheets, a strong job market, falling inflation, and real income growth. The robust financial health of households has been buoyed by gains in household wealth, particularly among high-income households. Additionally, consumer spending has been a significant driver of economic growth, accounting for almost 80% of real GDP growth in the first three quarters of 2024. The household debt service ratio is in line with pre-pandemic levels, indicating that consumers are managing their debt effectively. Wage growth, which surged coming out of the pandemic, has returned to a more normal rate of 4%, which is above the current rate of inflation. These factors collectively contribute to an above-average level of consumer confidence which is expected to continue supporting economic growth in 2025.

Key themes shaping our outlook

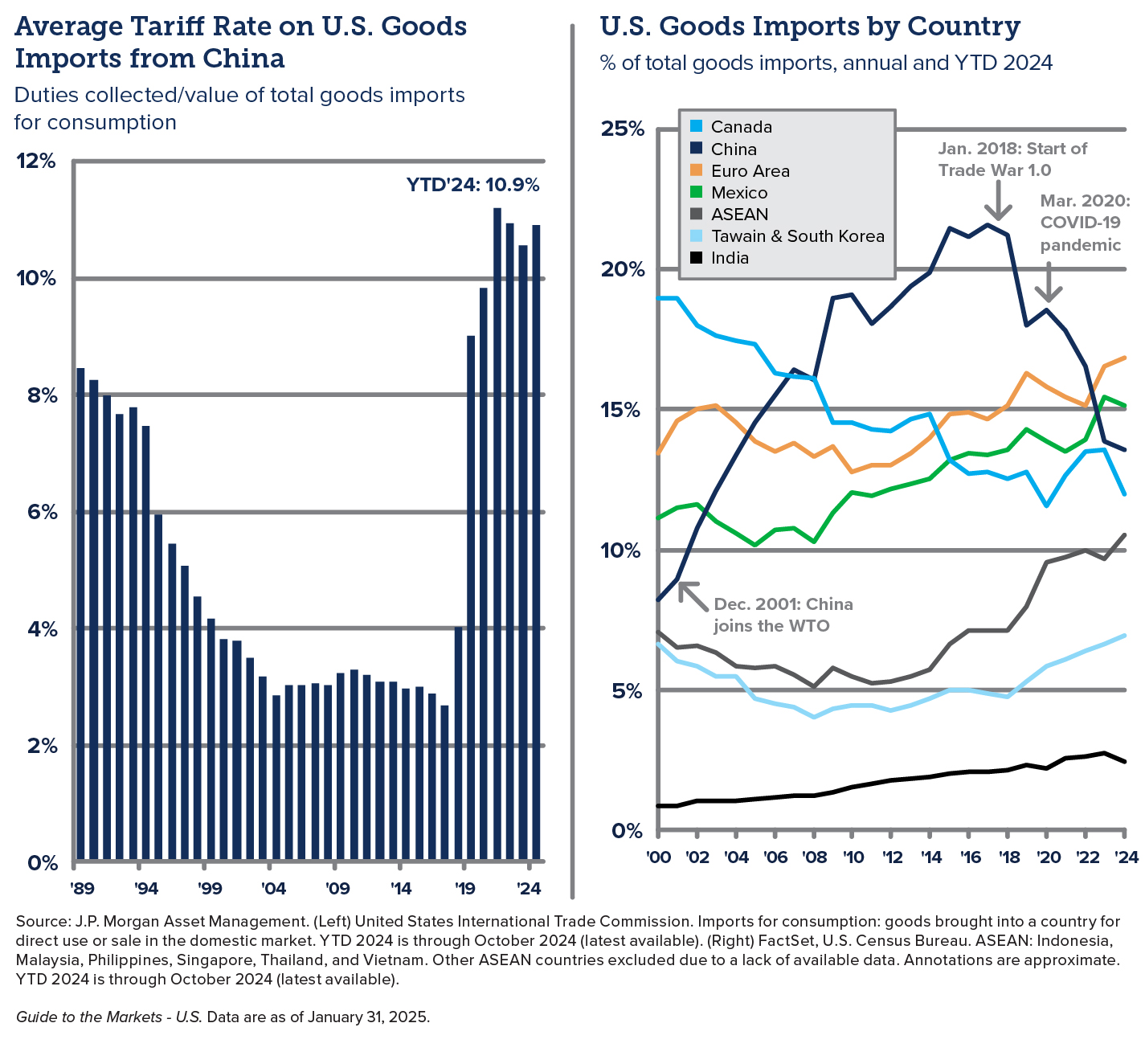

Tariffs

One of the most immediate issues that could affect the U.S. economy in 2025 is the proposed use of tariffs by the new administration. While the implementation of these tariffs may moderate from campaign rhetoric, a shift towards more protectionist measures is likely. The impact of these tariffs on inflation, as measured by the Personal Consumption Expenditures (PCE) index, could result in a temporary rise above long-term targets by the end of 2025. Retaliatory tariffs are also a strong possibility which could affect exports as countries turn to secondary suppliers.

Debt and tax policy

The large and growing federal debt will likely influence tax policy and proposed austerity measures. The new administration and Congress are expected to provide more clarity on the direction of tax policy with a full extension of the 2017 Tax Cuts and Jobs Act and the potential for lower corporate tax rates. While a reduction in federal debt in the short term would be difficult, reducing the annual deficit is a likely goal. Any cut to government spending is economically contractionary, so we expect the administration to attempt to balance any cuts with other policy measures to induce growth.

Global tensions

Global conflicts remain one of the largest unknowns in our outlook and recent significant developments have added to this uncertainty. China’s positioning to become a dominant global power could be hampered by an economic slowdown at home. Escalating tensions between Russia and Ukraine could draw more countries into the conflict, draining resources. Political instability in regions such as the Middle East, France, and South Korea adds to the uncertainty for investors. Global tensions and the potential for political realignment, especially with our closest trade partners, remains very fluid in 2025.

Deregulation efforts

Deregulation efforts by the new administration could have a significant impact on the U.S. economy, but these effects are likely to be limited to specific sectors and may take years to materialize. President Trump’s previous presidency focused heavily on rolling back government regulations to stimulate the economy.

As his new term continues to take shape, it’s worth examining the effects of his earlier efforts and what similar policies could mean for your finances in the future. For example, deregulation within financial, healthcare, and environmental spaces could save or cost money depending on the specific changes implemented. Looser financial conditions and deregulation could be catalysts to stronger business investment and spending in the near-term.

Labor and consumer strength

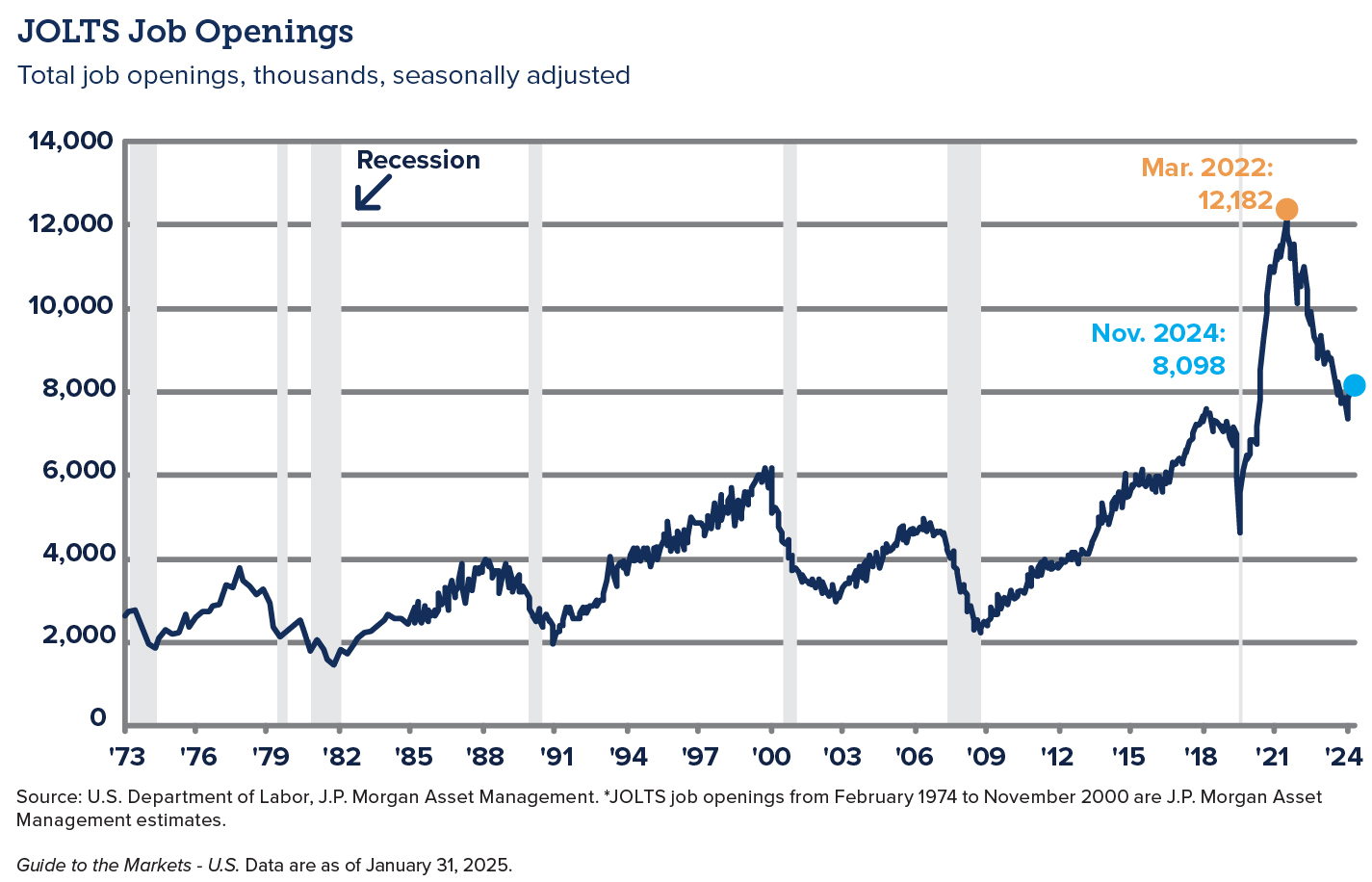

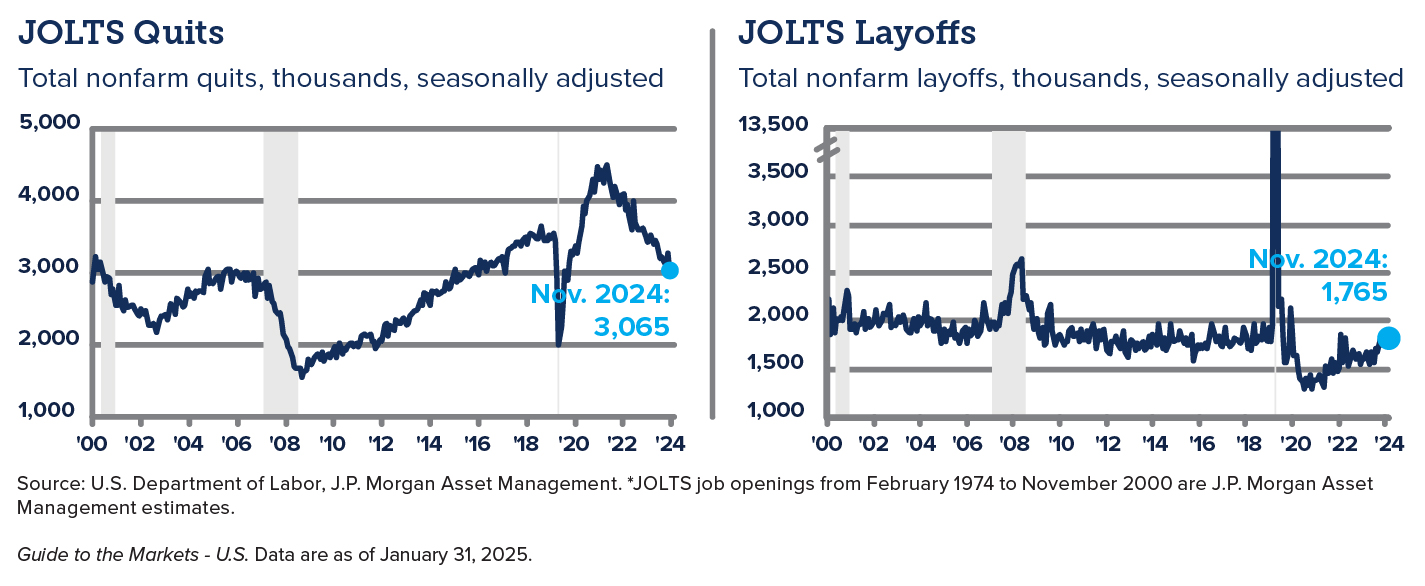

Consumer consumption, supported by high-income households, continues to drive economic growth, accounting for almost 80% of real GDP growth in the first three quarters of 2024. Business investment remains strong, supported by robust corporate balance sheets and fiscal support from legislation such as the CHIPS Act and the Inflation Reduction Act. However, higher borrowing costs will continue to pose a headwind to business investment. Curtailed immigration could decrease real economic growth by limiting labor force growth and potentially causing higher inflation through increased wages. Reshoring efforts, immigration reform, infrastructure growth, and advancements in AI could significantly impact labor supply and demand in some sectors.

Potential risks to our outlook

While our outlook for 2025 is generally positive, several potential risks could impact our projections. The proposed tariffs by the new administration could lead to retaliatory measures from other countries, affecting various sectors and potentially increasing costs for consumers. Inflation, driven by tariffs and other factors, could rise above long-term targets, impacting consumer spending and overall economic growth. Global tensions, such as the ongoing conflicts between Russia and Ukraine and political instability in regions like the Middle East, France, and South Korea, add to the uncertainty for investors. Additionally, the large and growing federal debt could influence tax policy and proposed austerity measures, potentially impacting economic growth. Finally, higher borrowing costs could pose a headwind to business investment, limiting the potential for economic expansion.

Regional economies

As with previous INTRUST Economic Outlooks, we take a closer look at our regional economies. We have a generally positive outlook for our markets, but economic hurdles are present and will provide some level of uncertainty.

The economic landscape in most of our markets is positive but is constrained by many of the same economic factors facing the rest of the nation. Tariffs applied by the US, and the potential for retaliatory tariffs, have a meaningful impact on our outlook in most of our regional economies. Supply chain disruption due to increased costs and/or source rerouting could have either a positive or negative effect on our regional economies depending upon the specific sectors targeted. Labor continues to play a significant role in the economic growth of our region with labor growth continuing to slow from its feverish post-pandemic pace. Employers in our region are benefiting from the relatively low cost of living in the Midwest but the influx of new families has increased the demand for housing, services, and infrastructure that is struggling to keep up with demand. Employee recruitment, as well as retention, will continue to play a key role in economic growth in both the short- and long-term outlooks.

As we look deeper into the economic projections for our regional economies, we include thoughts on impacts that may be realized, both positively and negatively, from the agenda of the incoming administration in Washington.

South Central Kansas

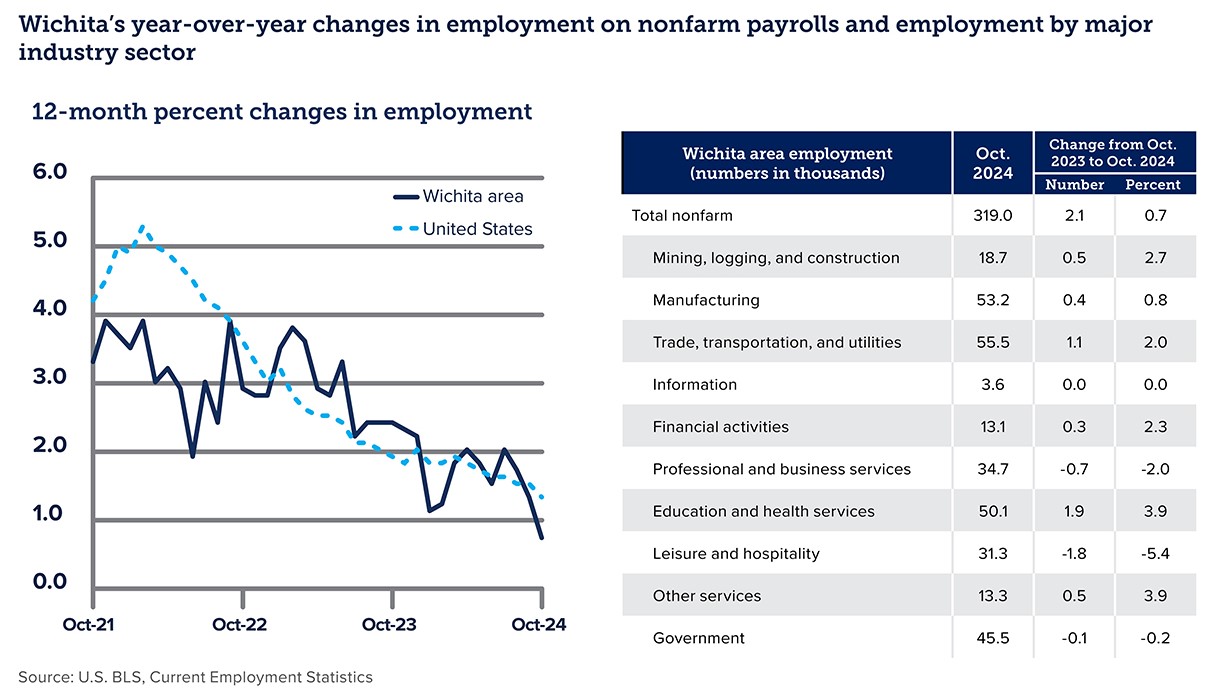

Wichita: We hold a positive outlook for the Wichita economy in 2025. Business and consumer confidence is strong, as housing and general construction activity increases and steady population growth is evident in our school districts. While demand remains high for skilled labor, supply is tight with the local market near full employment. Increased efforts in training and research are attracting new talent to the area, as evidenced by record enrollment at the Wichita Area Technical College and opportunity growth at the Wichita State University National Institute for Aviation Research (NIAR). Naturally, this continued demand for skilled labor supports wage and benefit improvements, which will strengthen the consumer balance sheet locally and support an attractive landscape for Wichita in 2025.

Newton and Harvey County: This area north of Wichita has a strong agricultural influence from both farming operations as well as the manufacturing of agricultural machinery. Low commodity yields hurt farm operations, which lead to a slowdown in purchase of operating equipment. Employment at some of the larger equipment manufacturers cooled in 2024, so attracting diversified businesses remains a high priority. The threat of tariffs, and the possibility of retaliatory tariffs, are a concern for this community as much of the economic output is sold overseas. A new manufacturing company and continued expansion of the services offered by the regional hospital should continue to fuel strong growth in this market as we move through 2025. Economic activity in Newton is closely tied to growth in Wichita as both communities expand, and this tie should strengthen as construction on key components of the I-135 corridor are completed.

El Dorado and Butler County: As the largest county in Kansas, Butler County has several unique communities and townships that deliver diverse economic opportunities from a variety of sectors, ranging from agricultural-based to manufacturing and business expansion. Holly Frontier Refinery, El Dorado’s largest employer, recently completed extensive upgrades to their facility and is running essentially at full capacity. In Andover, a 103-acre mixed-use development project known as The Heritage was recently completed, which has created significant momentum for future development.

As with many of our regions, immigration reform could negatively affect the construction industry, which has recently struggled to find, train and retain skilled laborers. Demand for affordable housing continues to be high as available housing stock is currently limited. Conversely, construction of large homes, primarily in and around Andover, continues to be strong as they continue to be highly desirable, and their demand has not been as significantly impacted by the higher interest rate environment as it has to entry and mid-level housing.

Northeast Kansas

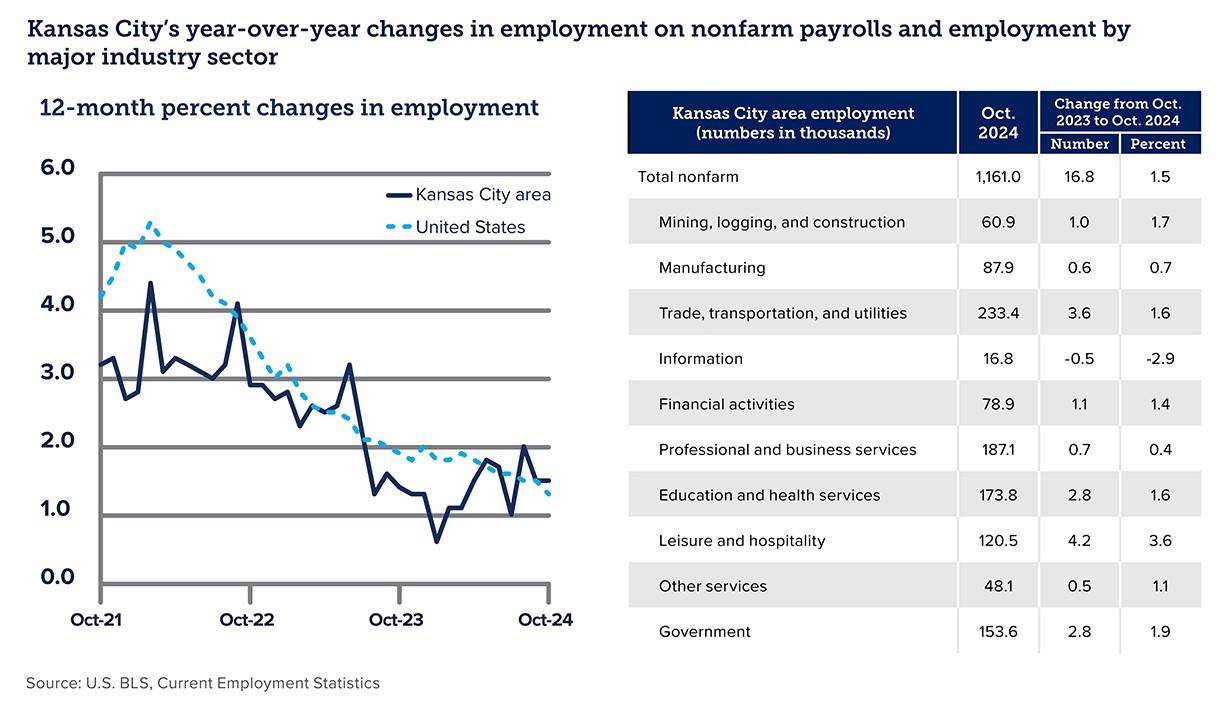

Kansas City/Johnson County: The greater Kansas City area boasts one of the most diverse economies in the Midwest, which should provide stable economic growth through 2025. Mergers and acquisitions (M&A) activity is increasing and streamlining from possible deregulation efforts could be positive. Increased economic activity is expected due to events unfolding in the KC sports landscape, including hosting the 2026 World Cup and new stadium plans for both the Royals and Chiefs.

Lawrence and Topeka: Both cities continue to benefit from the growth and stability of their universities, the University of Kansas and Washburn University, and are working to retain graduates through concerted efforts to attract new development. Topeka has recently received several different recognitions as one of the top communities in the nation and has poured resources into downtown revitalization. Proximity to the Panasonic plant in De Soto is fueling housing growth for Lawrence but will be a draw on tight labor resources as operations begin in mid-2025. Immigration reform could have a negative effect as the area is home to several construction companies and distribution centers that rely on a stable lower-skilled workforce.

Manhattan and Junction City: The economic climate in these communities remained stable through 2024, anchored by larger employers such as K-State University and Ft Riley. As with other communities in our region, housing remains tight as builders focus more on higher-end home construction. Manhattan Area Technical College has seen some growth, primarily in healthcare licensing and construction skills certifications. The possibility of tariffs would be seen as a headwind to the local economy. The significant agriculture-related operations, both in grain sales as well as machinery production, could be negatively affected by targeted tariffs and the probability of retaliatory tariffs from key trading partners.

Oklahoma

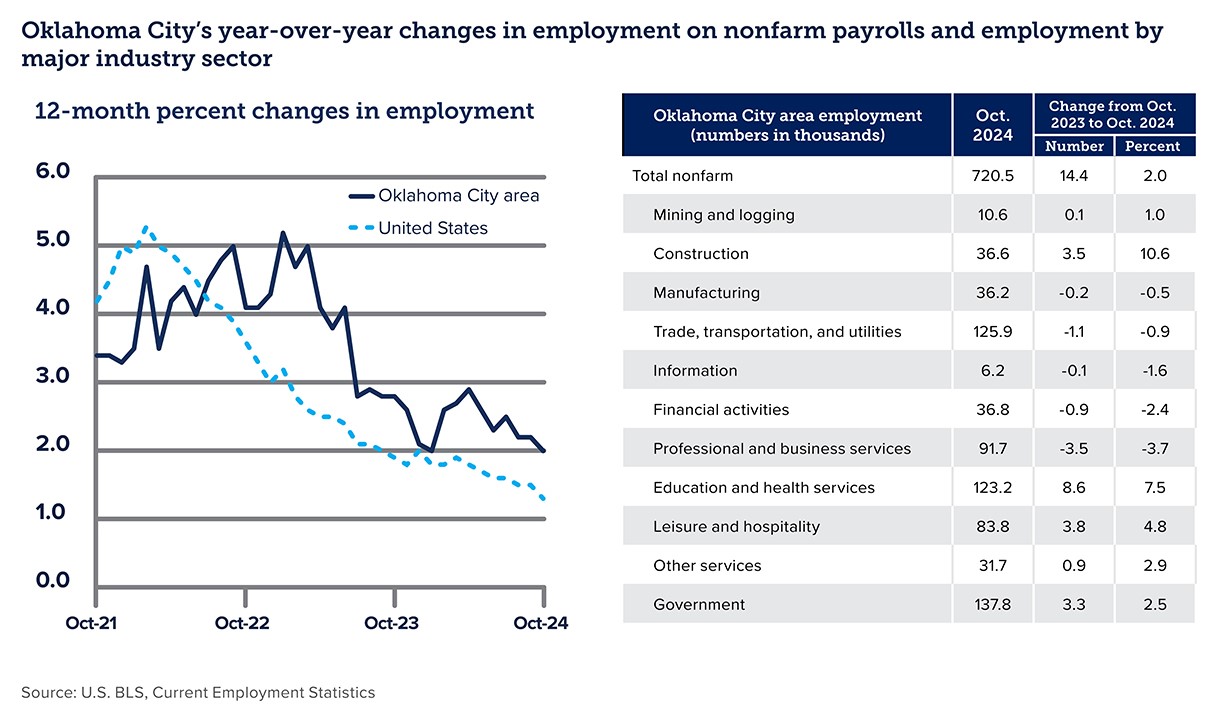

Oklahoma City: Economic growth in the Oklahoma City area continues to be robust, led by oil and gas activity and growth in the aerospace and biomedical industries. Oklahoma City has had success in their debt-free public improvement program funded by a temporary penny sales tax (MAPS program) that has funded several projects to enhance the quality of life and job-creating initiatives. Consumer confidence is high in this politically red state where some targeted tariffs and deregulation efforts would be viewed favorably. However, immigration reform could have a negative impact, primarily in the areas of construction and hospitality. Job growth remains above the national average and reductions in the potential workforce would limit economic growth to an extent.

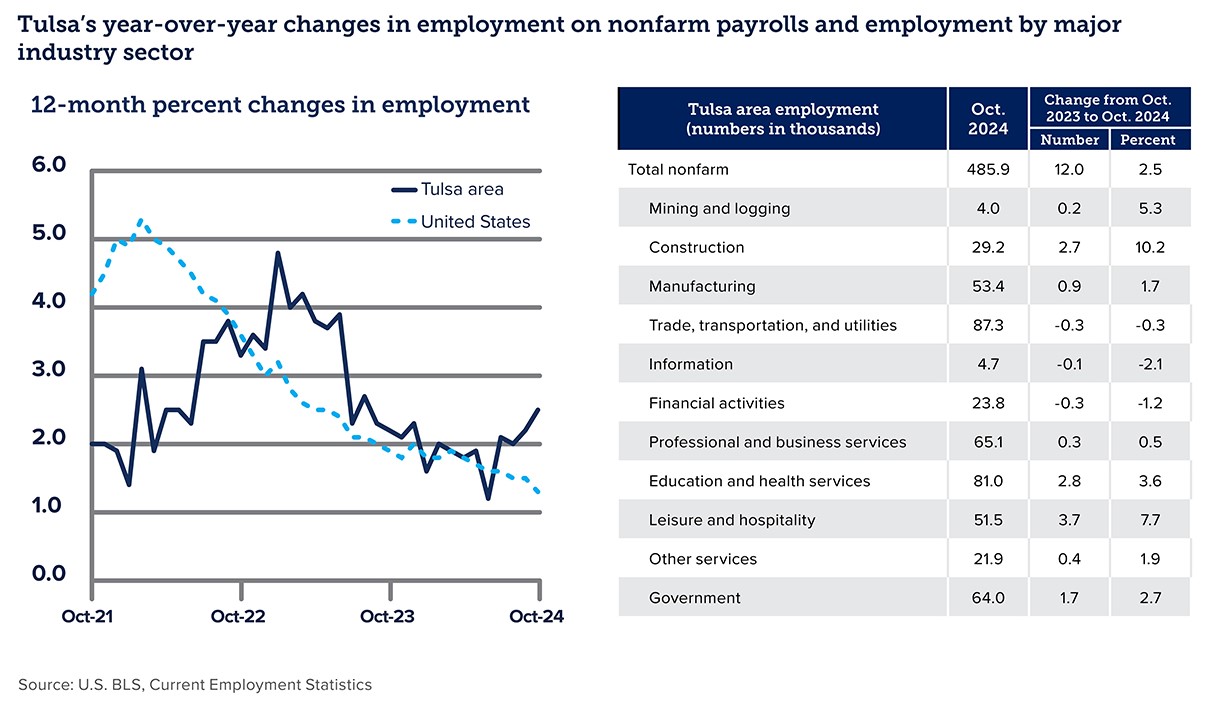

Tulsa: As an historically rich oil and gas economy, the Tulsa area continues to diversify into EV manufacturing, aerospace, and biomedical industries. Tulsa is also home to American Airline’s maintenance base – the largest of its kind in the world, as well as major aerospace companies such as NORDAM and Spirit AeroSystems. Transportation and logistics companies also play a key role in Tulsa’s economic footprint. Job growth continues above the national average average, and to attract more employees to the area, the George Kaiser Family Foundation is helping fund Tulsa Remote, a unique recruitment initiative that urges talented individuals and their families to consider Tulsa. The region would likely benefit from efforts to streamline oil and gas production as well as general deregulation. Our outlook calls for continued strong economic growth in the area, limited only by labor supply.

Northwest Arkansas

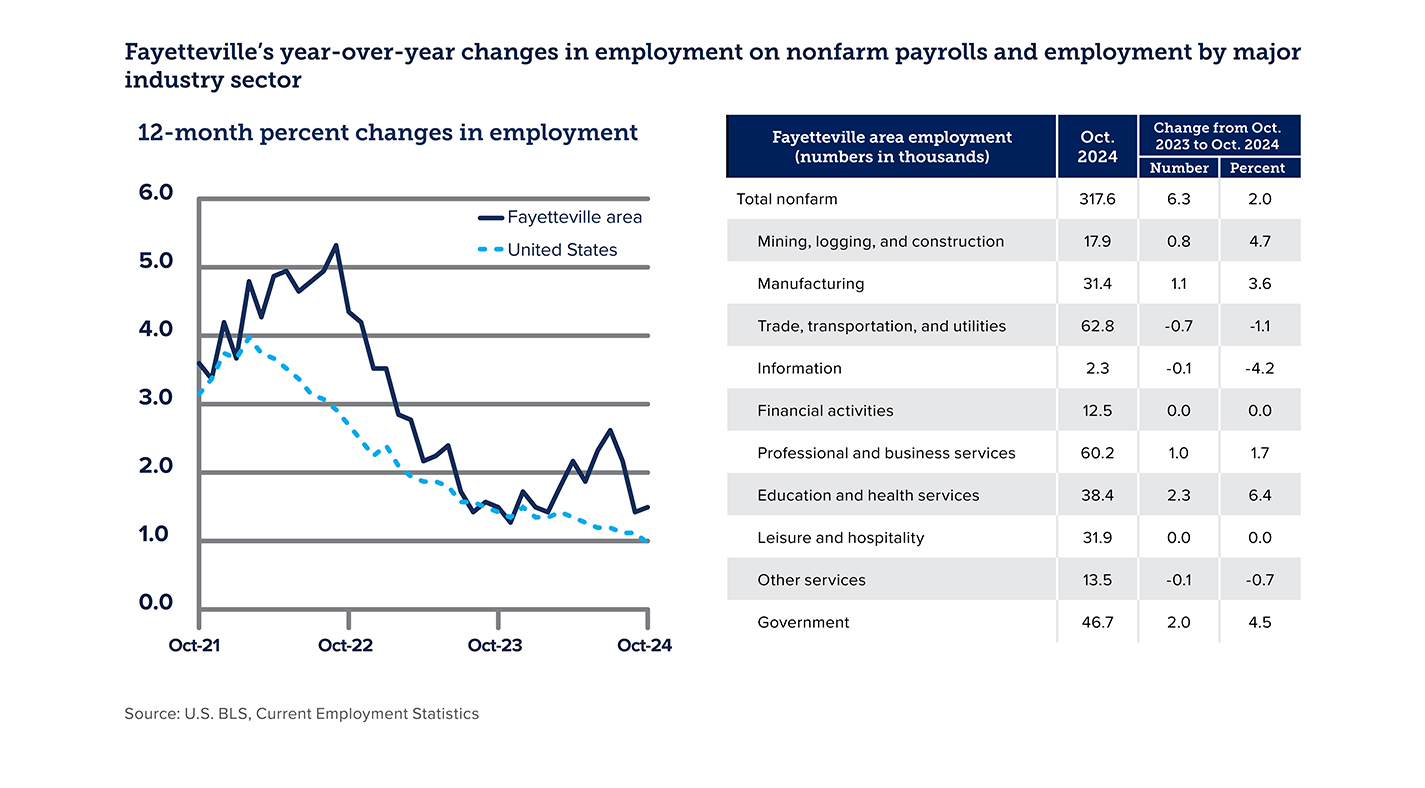

Economic growth in Northwest Arkansas (NWA) continued at a robust pace in 2024, fueling one of the largest employment percentage gains of the regions we serve. Quality of life and a relatively low cost of living is drawing both the workforce demographic as well as retiring Baby Boomers, the latter enticed by a quickly developing healthcare corridor. The area is home to the corporate headquarters of Walmart, J.B. Hunt, and Tyson, all of which are investing heavily in the local economy by bringing in additional jobs both directly and indirectly as they work to develop logistical economies of scale. Housing and infrastructure have been stretched by the rapid growth, but municipalities and businesses are working to stay ahead. Local builders are focusing on providing affordable housing and many larger businesses are building in capacity for childcare in an effort to attract and retain employees. Trade tariffs, particularly with China and Mexico, could result in diminished growth in the area. While the added cost of tariffs could ultimately be passed down to the consumer, Walmart and the more than 3,400 vendors in NWA that service Walmart would likely be squeezed in the process. Still, our outlook calls for continued above-average growth for NWA.

Investment outlook

Investment impact

Our overall outlook for U.S. corporate earnings growth remains positive, but sectors affected by potential tariffs could see weakness. Stabilized labor force supply and demand, particularly in sectors less affected by immigration reform, should help moderate corporate expenses. While protectionist measures may add costs, these could largely be passed on to consumers, which could lead to a slowdown in consumption, particularly in more discretionary sectors. Earnings growth through 2025 is expected to bolster broad-based market performance for equity holdings.

Equities

Equities have enjoyed two strong years of performance, rebounding from the 2022 downturn. This resurgence can be attributed to a combination of factors, including easing recessionary concerns and strong earnings growth. However, it is important to note that valuations have become stretched due to this strong performance, resulting in higher price-to-earnings ratios. Investors should be cautious of these elevated valuations, as they may limit the potential for further significant gains.

One of the driving forces behind the positive outlook for equities in 2025 is the expectation of strong earnings growth. Companies have demonstrated resilience and adaptability in the face of economic challenges, and their ability to generate robust earnings has been a key factor in the market’s recovery. Continued earnings growth is anticipated to support equity prices in the coming year.

The promise of deregulation has been a helpful factor for equities, creating a more business-friendly environment and reducing compliance costs. However, fiscal austerity concerns are hurtful, potentially limiting government spending and economic growth. Balancing these opposing influences will be crucial for sustaining market momentum.

Despite the positive outlook, there are still some concerns that could impact the equity markets. Tariffs continue to be a source of uncertainty, particularly in the context of international trade relations. Any escalation in trade tensions could have a negative effect on market sentiment and corporate profitability.

International stocks present an appealing opportunity for investors, with relatively attractive valuations compared to domestic equities. However, international economies are grappling with recessionary pressures, which could impact their market performance. Investors should carefully assess the risks and potential rewards of international investments. The strength of the U.S. dollar is another factor to consider when evaluating international equities. A strengthening dollar has muted international returns over the previous two decades, and it may continue to do so. Geopolitical tensions, trade disputes, and economic uncertainties can all create volatility and affect investor sentiment.

Fixed income

The Federal Reserve’s decision to cut interest rates by 1% in 2024 has set a favorable tone for the fixed income market. This monetary easing has provided a crucial boost, reducing borrowing costs and supporting economic activity. However, with inflation reducing slowly, the overall environment remains one of cautious optimism. The gradual decline in inflationary pressures suggests that interest rates may remain relatively stable, providing a supportive backdrop for bond prices.

The strength of the overall economy and robust employment figures are crucial underpinnings of the fixed income market. With a strong economy, the likelihood of widespread defaults diminishes, bolstering investor confidence. The resilience demonstrated by the labor market ensures continued consumer spending and corporate profitability, which bodes well for fixed income securities.

Credit spreads are currently tight, reflecting a positive sentiment in the market. The narrowing of spreads indicates a reduced perception of risk among investors, highlighting their confidence in the creditworthiness of issuers. As recession concerns subside, this optimism is expected to persist, further compressing spreads and supporting bond prices.

An area of potential concern is the heavy issuance of treasuries. Increased supply could exert upward pressure on yields, potentially challenging the fixed income market. Investors will need to navigate this dynamic carefully, balancing the allure of safe-haven assets against the impact of increased supply.

Corporate debt service ratios are stabilizing, reflecting the steady financial position of many companies. This trend is encouraging for the fixed income market, as it reduces the risk of defaults. In particular, high yield debt appears appealing given the current economic context. However, it is important to exercise caution with lower quality high yield debt, which may still pose significant risks.

Private capital

In 2025, the private capital market is expected to evolve with several notable trends. These developments will shape the landscape and create new opportunities for investors who are keen on navigating this dynamic sector.

Historically, businesses sought public listings to access capital and achieve liquidity. However, the current trend is for companies to remain private, focusing on long-term goals without the pressures of public markets. This shift allows them to refine their business models and scale effectively. For investors, this means they can benefit from the growth and value creation over a more extended period, translating to potentially higher returns.

Simultaneously, the private capital market is becoming more accessible to individual investors. Thanks to regulatory changes and advancements in technology, a broader range of individual investors can now participate in private investments. This democratization provides new opportunities for portfolio diversification and potential returns, allowing individuals to support innovative startups and high-growth companies that align with their investment preferences and risk tolerance.

Mergers and acquisitions (M&A) activity is anticipated to increase in 2025. Various factors, including favorable market conditions, abundant liquidity, and strategic growth needs, are driving this trend. Companies are increasingly seeking inorganic growth opportunities to expand their market presence and acquire new technologies. Private equity firms, with their capital resources and transaction expertise, are well-positioned to facilitate and participate in this wave of M&A activity.

Portfolio considerations

In light of the recent developments in the equity and fixed income markets, we are implementing strategic adjustments to our portfolios to capitalize on favorable market conditions while managing potential risks effectively. Given the robust economic fundamentals and strong employment figures, we are increasing our overweight position in U.S. equities. The solid economic backdrop and consumer confidence suggest a favorable environment for equity growth, particularly in the United States.

We are also moving our small cap weighting back to neutral. While small caps offer potential for high returns, maintaining a balanced exposure will help manage risk and ensure a diversified portfolio. Additionally, our underweight position in large cap equities is being reduced. Large cap companies, with their stable earnings and market influence, are well-positioned to benefit from the current economic environment. This adjustment will enhance our exposure to established, resilient companies.

Within the fixed income allocation, we will retain our current duration profile. Our short to intermediate duration profile will allow us to benefit from favorable bond prices while managing interest rate risk. We will continue to use active bond managers to navigate the dynamics of the fixed income market, especially given the potential challenges posed by previously. Our managers will be tasked with identifying opportunities and mitigating risks associated with increased supply and yield fluctuations. Similarly, our active high yield strategies will continue, as high yield debt appears appealing in the current economic context, yet we are exercising caution with low quality high yield debt.

These strategic adjustments reflect our commitment to optimizing portfolio performance while maintaining a prudent approach to risk management. We remain confident in our ability to deliver value to our investors and look forward to navigating the opportunities and challenges that 2025 will bring.

The INTRUST 2025 Economic Outlook is the consensus of the INTRUST Bank, N.A. (“INTRUST”) Investment Strategy team and is based on third party sources believed to be reliable. INTRUST has relied upon and assumed, without independent verification, the accuracy and completeness of this third party information. INTRUST makes no warranties with regard to the information or results obtained by its use and disclaims any and all liability arising out of the use of, or reliance on the information. The information presented has been prepared for informational purposes only. It should not be relied upon as a recommendation to buy or sell securities or to participate in any investment strategy. The forward-looking perspectives are not intended to, and should not, form a primary basis for any investment decisions. This information should not be construed as investment, legal, tax or accounting advice. Past performance is no guarantee of future results.

| Not FDIC Insured | No Bank Guarantee | May Lose Value |

Posted:

03/05/2025

Category:

Related Blog Posts